The most common question I hear these days is a variety of “Why isn’t the stock market reflecting the carnage in the broader economy?”. I broadly addressed this topic in a recent post but one part of that answer deserves a little more explanation.

Importantly, when people talk about “the stock market”, they are generally referring to the S&P 500 Index and/or the Dow Jones Industrial Average. These two benchmarks are ubiquitous and hard to avoid. Ask someone how the stock market did today and you will assuredly get a response that directly or indirectly references one of those two indices.

This 2016 article explains why the Dow is a terrible accident of history and that it is only history, name recognition, and habit that cause the world to continue using this index as a reference point. The other index that we collectively use to represent the stock market – the S&P 500 – is a far better representation of the domestic stock market. Yet it is far from perfect.

One big issue with identifying the S&P 500 Index as “the stock market” is that the S&P tends to be overwhelmingly influenced by a handful of large companies within the index. That concentration has never been more impactful, historically, than it is right now. Just five companies – Microsoft, Apple, Amazon, Facebook, and Google (Alphabet) – represent approximately 21% of the Index. The larger these companies get relative to the rest of the stock market, the more dominant of an influence they have on the index.

As a result, these five stocks skew our perception of how the stock market, in a broad sense, is performing. Consider, for example that cruise line stocks are down 70-80% this year. Retailers have generally lost 50%-65%. Oil and gas exploration and production companies are down 55% – 65%. These industries have justifiably been devastated by the pandemic but the devastation is being obscured by the way the index is constructed. While 14 stocks representing these industries have declined by an arithmetic total of 869% this year, their total impact on the S&P 500 is offset entirely by Microsoft’s 14% gain in 2020.

A similar phenomenon holds true for the airlines in the S&P 500 – all of which have lost between 50% and 74%. The aggregate decline of all the airline stocks in the S&P 500 during 2020 – an arithmetic loss of 311%- is entirely offset by Apple’s 4% gain.

This tends to be an important source of confusion when people question why the “stock market” is not depicting the carnage on Main Street, The reality is that most stocks are reflecting the harsh realities of the pandemic. Airlines, retailers, apparel makers, lenders, cruise lines, hotels, financials, automakers, leisure and entertainment companies, and oil and gas companies have all been devastated this year. As of May 20th, over 1/3 of the stocks within the S&P 500 have lost more than 27% of their value.

But that carnage is being masked within what we define as “the stock market” by the performance of five stocks that have a dramatically disproportionate impact and have, for different reasons, continued to do well amidst the pandemic. Just something to keep in mind the next time you’re confronted by someone who questions why the stock market isn’t reflecting the harsh economic realities of Main Street.

With the suspension of required minimum distributions (RMDs) in 2020 by way of the CARES Act, there’s a question that all individuals over age 70.5 need to be asking this year: Is it still more tax efficient to make charitable gifts from my IRA via qualified charitable distributions (QCD) even though there is no RMD to reduce or avoid?

As a quick refresher, the QCD (explained more fully in this Golden Bell article) was first authorized by Congress in 2006. It lapsed and was reinstated five times over the coming years only to become permanent in 2015. Regrettably, consumers barely took notice of this useful tax strategy until the Tax Cuts and Jobs Act which dramatically changed the tax law starting on January 1, 2018. Despite its lack of use and appreciation, the QCD is not a complex tax planning strategy that only applies to a small fraction of taxpayers. It permits any taxpayer over age 70.5 to make IRA distributions directly to a public charity without treating the distributions as taxable income1. Save for taxpayers over age 70.5 who retain a large primary residence mortgage into their 70’s or those with unusually large medical expenses, nearly all taxpayers with a Traditional IRA will reduce their overall tax liability by fulfilling charitable gifts via the QCD rather than by other methods such as giving cash or appreciated securities.

The QCD calculus changes in 2020 because of the RMD suspension enacted by the CARES Act. In normal years, when taxpayers have a required minimum distribution and fulfill some or all of their RMD by use of the qualified charitable distribution, they reduce adjusted gross income dollar-for-dollar by the amount of the QCD. Although there are a few scenarios where this may not be advantageous in the long term2, reducing adjusted gross income generally results in a reduction in taxes which makes the QCD advantageous for most taxpayers over age 70.5.

Making charitable contributions via the QCD in 2020 does not reduce 2020 taxes because there is no RMD that the QCD is replacing.3 However, fulfilling charitable donations in 2020 by using the QCD in lieu of giving cash or securities still has a favorable impact on future taxes because the taxpayer reduces IRA assets which inherently have a deferred tax liability. A taxpayer who faces a 22% marginal tax rate, for example, and donates $100,000 from his IRA via the QCD, has just eliminated $22,000 of future tax liability (for him, or for his beneficiaries, assuming the same 22% tax rate applies).

To evaluate the tax impact of the QCD in 2020, we can compare the value of this reduction in future taxes via the QCD to the alternative of donating cash or appreciated investments which may have present and/or future tax benefit. Let’s start with the following baseline scenario: Jill is age 75 and has $1 million of IRA assets and $1 million of after-tax assets. She gifts $10,000 per year to charity and requires another $70,000 per year in after-tax dollars from her financial assets for living expenses. Jill’s 2020 dilemma is whether she donates the $10,000 to charity from her IRA via the qualified charitable distribution or whether she gives the gift from cash or appreciated assets.4

QCD vs. Cash Donation

In the case where Jill is contemplating a gift of cash to charities in 2020 and will claim the standard deduction on her tax return, using the QCD is a decided no-brainer. By using the QCD instead of cash gifts, she will have an additional $3,745 of after-tax wealth at age 90 just for having donated the $10,000 from her IRA rather than from non-IRA assets. To the extent that she has beneficiaries who inherit her IRA at age 90 and who will be taxed on the distributions at a higher rate than her (32% vs. 22%), the benefit of using the QCD in 2020 is even greater – a $4,598 increase in cumulative after-tax wealth.

Let’s now change the scenario to assume that Jill gets some benefit from donating cash in 2020. Specifically, we can assume that Jill would take the standard deduction if she uses the QCD but if she makes a cash gift, she is able to deduct 50% of the value of the donation (the first $5,000 of the donation gets her to the standard deduction amount and the next $5,000 increases her itemized deductions). Even under this scenario, Jill comes out ahead in the long-run by using the QCD. She saves $1,100 on her 2020 tax liability (22% tax rate x $10,000 gift x 50% of gift increasing itemized deductions) by making cash gifts but foregoing the QCD results in higher future taxes. Despite the $1,100 advantage in year one, her total wealth is still $1,627 lower at age 90 by giving cash rather than utilizing the QCD.

The table below shows that only in the scenario where Jill is able to deduct every penny of her charitable gift (likely because of high mortgage interest expense) and where her beneficiaries are in the same tax bracket or a lower tax bracket when they inherit her IRA, is she better off giving cash rather than using the QCD.

QCD vs. Donating Appreciated Investments

A better solution to donating cash is using appreciated investments for charitable donations5. Donating appreciated assets qualifies for the same deduction as a cash gift6 and results in the avoidance of future capital gains taxes when the assets would have otherwise been sold. While making charitable donations in 2020 with appreciated investments is better than donating cash, it is still suboptimal to utilizing the QCD for all scenarios in our example except when the taxpayer gets the full gift value benefit of an itemized deduction. We evaluated Jill’s situation using different levels of pre-existing investment appreciation and show the results below.

Summary

One important thing to note here is that we have evaluated a few very specific situations and, as with nearly all financial planning decisions, the individual circumstances matter to the calculation. There are a number of variables that could impact the economics including whether the individual desires to leave assets to charity at death, the expected rate of return on investments, the age of the individual, the expected spend rate of the individual, and how quickly or slowly the ultimate beneficiaries will distribute any inherited IRA assets. That said, in working through the economics of this decision using many different variables, there is one consistent conclusion: using the QCD for charitable gifts in 2020 is almost advantageous except in situations where the taxpayer can fully deduct or near-fully deduct the value of the donation.

The relatively brief history of qualified charitable distributions (QCD) goes back to 2006 when Congress first authorized the QCD in the Pension Protection Act – but only for two years. It lapsed in 2008, 2010, 2012, 2014, and 2015, only to eventually be reinstated each time. In late 2015, Congress permanently reinstated the QCD. It was not until the Tax Cuts and Jobs Act of 2017 (TCJA) that consumers really started to take notice of the QCD. By dramatically increasing the standard deduction and limiting the deduction of state and local taxes, the TCJA significantly expanded the pool of QCD beneficiaries. Although public awareness of the QCD has grown since then, we find that many consumers are still not aware of the QCD or just do not understand the simplicity and benefits well enough to put it to use.

What is the Qualified Charitable Distribution?

Despite its lack of use, the qualified charitable distribution is not a complex tax planning vehicle or a tax strategy that only applies to a small fraction of taxpayers. The QCD rule simply permits taxpayers over age 70.5 to make IRA distributions directly to a public charity without treating the distributions as taxable income. That is, money goes directly from the IRA to the charity without passing go.

How Does the Qualified Charitable Distribution Work?

In the 1040 example below, note line 4. Under normal circumstances, this taxpayer with a $35,000 required minimum distribution reports 35,000 on line 4a (IRA distribution amount) and then the same 35,000 on line 4b (taxable amount). In this example, the taxpayer directed all of the $35,000 required distribution to charity which, in turn, meant that line 4b – the taxable amount – was $0. This has important ramifications, which will be explained later.

What are the Requirements of the Qualified Charitable Distribution?

There are several important (but easy to fulfill) qualifiers:

The owner of the IRA must be at least age 70 ½ at the time of the distribution.

The distribution must go directly to a public charity (not a donor advised fund or private foundation).

The distribution must come from an IRA. Distributions from a 401(k) or 403(b) are not eligible.

There is no minimum QCD amount but there is a $100k limit per individual taxpayer. Note that a married couple, both over age 70.5, each qualify for the $100k limit so they would be able to use up to $200,000, in aggregate.

What are the Tax Benefits of the Qualified Charitable Distribution?

Without the QCD, a taxpayer would take his or her required minimum distribution (RMD), donate the amount of the distribution to charity, and then take a charitable deduction to offset the income. In some cases, this would result in a perfect offset and no net impact to the tax liability. However, with more than 90% of taxpayers now claiming the standard deduction and many of the remaining taxpayers losing some of the itemized deduction benefit because of the increased standard deduction, the offset tends not to be dollar-for-dollar.

What is the Primary Benefit of the Qualified Charitable Distribution?

Some examples will help to answer this question.

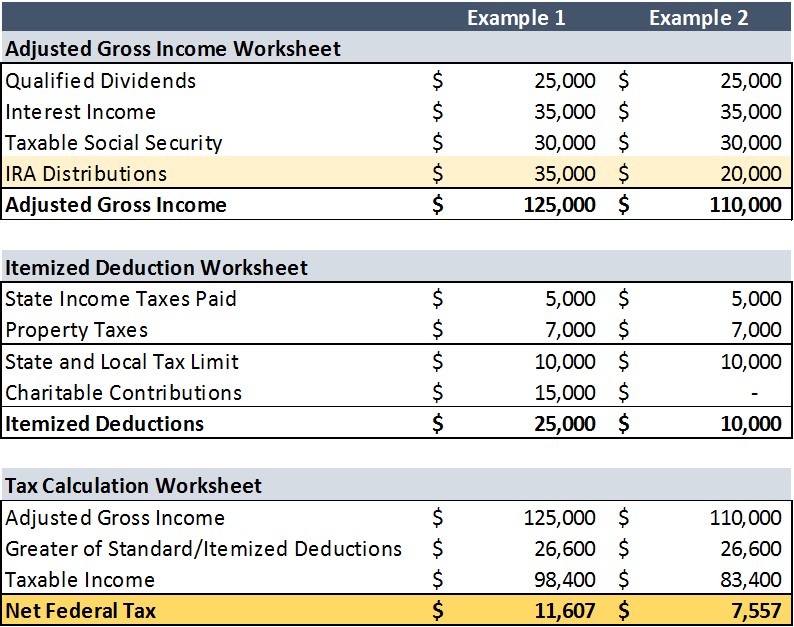

Example 1: Consider the case of a 72 year-old married couple, Jack and Diane, who have taxable Social Security income, dividends, and interest of $90,000 plus another $35,000 of required minimum IRA distributions from Jack’s IRA for total adjusted gross income of $125,000. They pay $5,000 of state taxes and $7,000 of property taxes, and have no mortgage or major medical expenses.

This year, they moved $35,000 from Jack’s IRA to their joint bank account to fulfill the required minimum distribution. Later in the year, they will write a check from their bank account for $15,000 to their favorite charity. Based on all their income and deductions, they will owe $8,444 in federal taxes.

Example 2: Now, assume everything stays the same except for the way in which Jack and Diane make their $15,000 charitable gift. Instead of moving $35,000 from Jack’s IRA to their bank account, they move $20,000 from the IRA to their joint bank account. Additionally, they give the same charity the same $15,000 but these funds come directly from the IRA. That is, the charity gets the $15,000 check directly from Jack’s IRA instead of going from Jack’s IRA to the bank account and then to the charity.

Financially, nothing changes for Jack and Diane and nothing changes for the charity. Check that – one thing changes for Jack and Diane. Instead of paying $8,444 in taxes in our initial example, they pay $6,644 in the second case. Their tax liability drops by $1,800 or 21.3% simply because they were wise enough to make use of the qualified charitable distribution.

What caused this significant reduction in federal taxes? In example 1, Jack and Diane made $15,000 of charitable contributions but they did not get any benefit from these contributions because their total itemized deductions of $25,000 were less than their standard deduction of $27,000. Had they given away $5,000, $10,000, or $15,000 or zero to charity, they would have faced the exact same federal tax liability.

In the second example, because they made the gift directly from their IRA and utilized the qualified charitable distribution, what would have been a taxable $35,000 mandatory IRA distribution was reduced to a $20,000 taxable distribution. In turn, their adjusted gross income and taxable income in example 2 were both $15,000 lower than in example 1. Yes, their itemized deductions were also $15,000 lower because they didn’t get to claim any charitable contributions but that’s the whole point. Reducing their income by $15,000 was far more valuable than increasing their itemized deductions by $15,000.

A married couple without major medical expenses or without a primary mortgage interest expense that exceeds $17,000 per year are likely to benefit from utilizing the qualified charitable distribution for the same reasons as Jack and Diane. It is a tax savings tool, unavailable to anyone under age 70.5, that effectively allows for the shifting of charitable deductions from the Schedule A, where they may not be entirely useful, to the front page of the Form 1040, where they’re going to be useful for anyone who pays taxes.

Who else might benefit from the QCD?

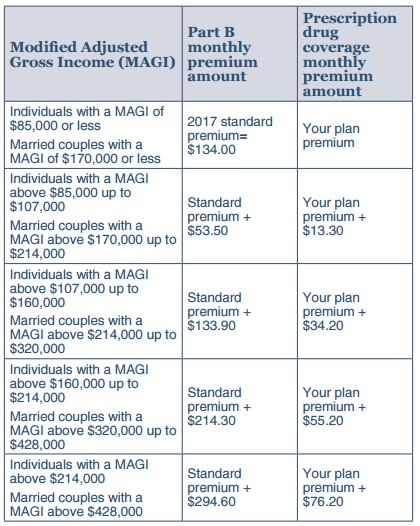

Couples with more than $170,000 of modified adjusted gross income and individuals with more than $85,000 of income can use the QCD to avoid higher Medicare premiums.

Medicare B and D premiums are tied to the modified adjusted gross income (MAGI) of taxpayers. Single taxpayers with modified adjusted gross income of more than $87,000 and married filing jointly taxpayers with MAGI of more than $174,000 pay an additional Medicare premium amount, known as income related monthly adjustment amounts (IRMAA). For example, a married taxpayer with modified adjusted gross income of $174,001 would pay an additional $115.60/month or $1,387/year compared to a couple with $174,000 of income – just $1 less.

The income thresholds in the leftmost column above are based on modified adjusted gross income – which means they are not reduced by itemized deductions (i.e. charitable gifts). A married taxpayer with $175,000 of adjusted gross income who donates $10,000 to charity via checks has to pay the higher Medicare premiums. However, if the same taxpayers use the QCD to donate the same $10,000 to charity, MAGI is reduced to $165,000 and the tax filer does not face the additional Medicare premiums – a simple and quick one year tax savings of $1,387.

Married tax filers with over $250,000 of AGI or single filers with over $200,000 of AGI can use the QCD to reduce the 3.8% Medicare tax.

The 3.8% Medicare tax on investment income only applies to married filers with more than $250,00 of AGI or single filers with more than $200,000. Utilizing the QCD technique can either relieve taxpayers of that tax completely by reducing AGI below those levels or can reduce the amount of investment income that is subject to the 3.8% tax.

For example, a taxpayer with $50,000 of charitable contributions who is subject to the 3.8% Medicare tax on $125,000 of income beyond the thresholds can save $1,900 in taxes ($50,000 x 3.8%) by simply making use of the QCD.

Rental property owners who actively participate in the property’s rental activity can use the QCD to qualify for a larger taxable rental loss.

If you own a rental property and meet the requirements to qualify for active participation (make management decisions related to the property, etc.), the tax code allows you to deduct up to $25,000 of rental property losses each year. Importantly, to claim the rental losses as an offset to other income, your AGI must be below $150,000 (or $75,000 for single filers). Since the income threshold is determined by AGI and not by taxable income, this presents another opportunity for the QCD to reduce income and, resultantly, to allow the taxpayer to claim a larger tax loss.

Tax filers who receive Social Security and have limited other income sources can use the QCD to reduce or eliminate the amount of Social Security that is subject to taxation.

The IRS looks at something called “combined income” to determine how much of your Social Security will be subject to taxes. Combined income consists of AGI (less Social Security) plus tax exempt municipal bond interest plus ½ of Social Security benefits. If your combined income is below $44,000 (for a married couple; or $34,000 for a single individual), then the amount of Social Security subject to taxation is reduced. Anyone close to these thresholds could benefit from utilizing the QCD to reduce combined income.

Tax filers who are constrained on the size of their charitable deduction can use the qualified charitable distribution to realize a larger tax benefit from their charitable giving.

For taxpayers who itemize deductions, the IRS limits the size of the charitable deduction to no more than 50% of adjusted gross income and, depending on other factors, sometimes 30% or 20% of AGI. As a result of these limits, taxpayers who make large charitable gifts each year can have their deduction limited. The QCD allows taxpayers to make charitable gifts without being subject to these limits.

Closing Comments

Importantly, none of the advice above suggests giving more dollars to charity simply for tax benefits. The amount of charitable giving is a personal decision that should not be determined or driven by potential tax savings. However, the method of gifting can often be optimized to have a profound impact on the tax benefit of the gift.

The intent here is not to suggest that the qualified charitable distribution has benefit for all individuals who are over age 70.5. In fact, the QCD is not going to be of any value for some tax filers. Individuals who do not make charitable gifts, who don’t fit any of the criteria above, or have large, low basis stock positions are likely not going to benefit from the QCD.

Instead, the intent here is to expand awareness on what the QCD is, how it works, and how you might benefit from its use. Simply understanding that it exists and how it can be utilized likely separates you from the majority of Americans.

The economy just lost 30 million jobs over the past six weeks – an incomprehensible figure that likely understates the actual damage because of slow and archaic state processing. The White House warned that unemployment could reach 20% by June. Real GDP fell by an annualized 4.8% in Q1 and forecasts suggest annualized real GDP could contract by roughly 40% in Q2. Consumer spending – the lifeblood of the economy – suffered its worst monthly decline (-7.5%) since measurement of this metric began in 1959. The Federal Reserve Chairman described this economy as “the worst ever”.

Oh, and the stock market just enjoyed its best month in more than 30 years and its third best monthly return since World War II. Of course it did.

How does this make any sense? Have investors lost their minds? When is the stock market going to wake up and catch up with all this horrific data? Why are stocks going up when the economy is not getting better – it’s getting worse? Why not get out of stocks and wait until the stock market catches up with the economy? What in the world is going on here?

Do not despise if you have asked yourself one, some, or all of these questions over the past several weeks. Look, the stock market does not make sense at times. And that statement alone should be reason enough to avoid trying to “time the stock market”. But you should also appreciate that a lot of what happened in April does make sense. It makes a lot of sense if you step back and appreciate how the stock market works. It makes sense if investors embrace the truth that the stock market does not behave like they think it behaves.

So, let’s step back and collectively address all the questions above as one: Why did the stock market rally in April?

Reminder: The stock market already plummeted based on the dire forecasts. Remember March 2020? In a 23-day stretch that began in late February, the stock market plummeted by 34%, marking the fastest bear market ever. This happened – mind you – while the unemployment rate (3.5%) was at its lowest level since 1969 and while weekly unemployment claims were near their lowest level since the 1960’s. The first blip in the weekly unemployment claims – 3.3 million new claims – was reported on March 26, 3 days after the stock market reached its nadir and was already recovering.

What’s that you say…the employment data was lagging and the stock was out in front of it? Exactly the point. The stock market sold off in anticipation of the lousy data that we would get in April and May and June and July. You know…the data that we actually got last month.

Reminder: The stock market only cares about today’s data that reflects yesterday’s news if it impacts tomorrow’s outlook.

April was the best month for stocks in more than three decades because the dramatic uncertainty we faced in March became less uncertain in April. Uncertainty did not go away. It never does. It was just that the extreme range of possibilities we faced in March became less extreme. The curve flattened. Covid-19 cases did not go to zero but we also were not experiencing over 1,000,000 new cases a day – which was a real possibility in March. Suggesting that the stock market needs to catch up with the economy completely misses the point.

Reminder: The stock market reflects large publicly traded companies in many different industries making profits in many ways.

Are most companies impacted by Covid-19? Without a doubt. However, the impact of this pandemic is clearly different for Microsoft than for Delta Airlines. It is different for Amazon than it is for Gap. And the stock market eventually baked in the differentiated impact of this pandemic. So, while the stock market may have recovered some of the losses in aggregate, it is worthy of reminder that cruise line stocks are down 70-85% since the beginning of the year; that oil and gas companies are down 50-70%; and that most brick-and-mortar retailers and airlines are down 50-70%. This is to say that the stock market is behaving like it is supposed to behave – dramatically penalizing the companies that have been and will be most negatively impacted by the coronavirus – a reality that gets lost in the aggregate.

Reminder: Investors were panicked in March. They behaved like panicked people behave.

This is a blurb from the Golden Bell Financial investment commentary to clients on March 11th:

“One underappreciated yet important item of note is that the selling during these past three weeks has been largely indiscriminate – a sign that investors aren’t being entirely rational. Stocks of companies with less debt or better cash flow that should be better prepared to weather an economic storm have sold off more than the companies with heavy debt loads or weak balance sheets. Most of the ugly selling days have been a sell-first, ask-questions-later environment where fear dominates and the institutional investors are just selling what they can get out of easily. That creates opportunity for patient, long-term investors who are not forced to sell.“

It is hard to say how much of the recent recovery in stocks has simply been the result of the fear and panic subsiding but it is clearly a component of the recovery. That is how this tends to work – panic causes irrational selling where prices fall based on deteriorating fundamentals but they go below the intrinsic, fundamental value because of the fear. Eventually, the fear subsides and prices find their fundamental value. This is the stock market’s way of transferring wealth from individuals who wait on the sidelines “for things to calm down” to investors who stay disciplined. Investing in the stock market is not a free lunch and it is the scary periods that provide the reward for the disciplined investors. That reward just came really quickly this time.

Reminder: The impact of monetary and fiscal stimulus cannot be overstated.

It is difficult for households to fully appreciate how monetary and fiscal stimulus impacts the economy because we are used to a reality where job loss or loss of income means that a family can’t spend as much, has borrowing sources cut off, and struggles to pay bills. That’s the reality a family faces. But in in an economy where the government can borrow more at extremely low rates or print more dollars to buy goods and stimulate demand, the household constraints don’t apply. The unprecedented levels of stimulus we have experienced since mid-March – both fiscal (Congress) and monetary (Federal Reserve) – are likely to have an enormous impact on the economy – a point that does not get anywhere near the attention it deserves from individual investors.

Many readers are now saying, “Yes, but all this borrowing and printing of trillions of dollars has a cost.” To be clear, it does. This is not a free lunch. What the current stimulus effectively does is pull forward future growth and future demand into the present resulting in higher stock prices today at the likely expense of tempered future economic growth and compressed returns (for not just stocks but also cash and real estate and bonds) over the next 10-20 years. In this case, consuming too much on Friday night doesn’t necessarily result in a terrible Saturday morning hangover – it more likely results in a sluggish week to follow.

Reminder: Relying on any “expert” predictions about the future is foolish.

This really does not address the initial question and seasoned clients are tired of hearing it. However, it is important to note: Save for some “market prognosticator” who publishes daily market predictions to his nine Twitter followers and who correctly called 14 of the past 1 bear markets, no economists or forecasters or equity strategists predicted the dramatic impact that Covid-19 would have on the economy and the stock market in March. In the same vein, no forecasters or equity strategists predicted the immediate and robust stock market recovery we would experience in April. Just another reminder of the value of forecasts.

Look, the stock market is unpredictable and sometimes confounding. If it was easily predictable and always made complete sense, long-term stock returns would look more like long-term cash returns. But all told, the stock market makes a lot more sense than investors give it credit for.