In the microeconomic environment of a single household, we make regular decisions about how much of an item or service to purchase. These decisions tend to be driven by our needs, our preferences, social norms, limitations, or by the price. We might purchase eight bananas at the store based on how many we expect to consume or 16 gallons of fuel based on capacity limits. We might purchase a house based on how much we can afford or tip an Uber driver based on social norms.

Individuals are faced with a similar dilemma when it comes to portfolio construction. Consider one of the most foundational decisions: how much should an investor allocate to foreign stocks? The only limitation is the amount of money available to invest. There is no consumption preference to guide this allocation decision or a fundamental “need” for any foreign stocks. How best to determine the amount to allocate to foreign stocks?

Because of the importance of this decision, it merits a robust decision framework rather than a glib gut-feeling or rule of thumb. We start below with the justification for foreign diversification and then summarize the framework for how we think about the foreign stock decision and the appropriate target level.

The Benefit of Foreign Diversification

The fundamental argument for diversifying to foreign markets is not that foreign countries are less risky or that they experience higher growth or have higher expected returns. The benefit is that foreign markets experience different ebbs and flows and these differences result in a significantly smoother portfolio result. There are different risks in the Swedish stock market or different factors impacting stocks in Brazil. Diversifying the risks, the factors driving returns, and the ebbs and flows results in a smoother ride. It’s more than just theoretical. The chart below demonstrates, based on historical evidence, the reduction in volatility by adding foreign equities to a portfolio of US stocks. Notably, the greatest benefit over this period of more than five decades comes from 40% foreign equity exposure.1

The same benefit is evidenced by historic risk-adjusted returns where the optimal allocation for an all stock portfolio over the same time period (Jan 1970 – May 2020) was 55% US stocks and 45% foreign stocks (based on the Sharpe Ratio – a useful measure of risk-adjusted returns)2.

Not only does this addition of foreign stocks dampen the volatility over the stretch of more than 50 years, it also increases the return as evidenced below with the addition of 40% foreign stocks to a US-only portfolio. This win-win outcome is the quintessential benefit of diversification.

How Much Diversification?

Historical evidence over the last 50 years suggests that an allocation of 40-50% to foreign stocks results in the highest risk-adjusted returns in an all-stock portfolio. Another way to evaluate the appropriate allocation to foreign stocks is to start from a humble place with the admission that the stock market reflects all available information and the best estimate of the right price. Based on this foundation, we can simply use the aggregate value of all stocks in all markets around the globe – the global “market capitalization” – as a reflection of how collective wisdom values the appropriate size of the US market relative to foreign markets.

Based on the market capitalization approach, US stocks represented 55.6% of the global market at the end of 2019.

Everything up to this point suggests a foreign stock allocation of somewhere between 40-50% in an all-stock portfolio. But there are pertinent justifications to consider deviating from that weighting.

The Case for Overweighting Foreign Stocks

The Supply/Demand Distortion of Home Country Bias – One of the most well-documented behavioral mistakes that investors consistently make is the tendency to favor investments from their own country – termed “home country bias”. It is a derivative of familiarity bias – our inherent tendency to favor what we know best – the reason that people who frequently fly Delta overinvest in Delta stock or that people who work for Southern Company overinvest in Southern Company stock. US investors are more familiar with US companies and so they overinvest in US stocks. And it is not just US investors. This bias invariably exists in every country around the globe. The data below from a 2017 Vanguard study reflects a few examples.

Because of the large size of the US relative to every other country, the home country bias creates a distortion that results in excess demand for US stocks and excess supply of foreign stocks.3. As a result of home country bias and this supply/demand distortion, US stocks are inherently overvalued (reducing the expected long-term returns) and foreign stocks undervalued (increasing the expected long-term returns). This dynamic can be expected to persist as long as home country bias remains and as long as the US investment market remains significantly larger than the rest of the world.

US Residents are Overexposed to the US, Outside Their Portfolios – Most US residents investing in stocks have a job in the US, own a house in the US, and will receive Social Security from the US government. That is to say that if we consider the broader portfolio of US residents, most – if not all – of their real estate and human capital wealth is tied to the US. If the US market does well, US residents are likely to see appreciation in their home values and better job security and/or compensation. The opposite is also true. As a result, there is a strong argument that US residents should increase foreign exposure in their financial portfolios to better diversify their domestically-concentrated non-financial portfolio.

Valuation – The strongest case for overweighting foreign investments – albeit a potentially temporal one – is valuation. Robust evidence across sectors, countries, asset classes, and time periods clearly indicates that starting valuation is the best determinant of future returns. One example is evidenced below – showing the cheapest periods of US stock valuation on the left to the most expensive periods on the right and the subsequent 10-year returns.4

US stocks today are expensive by nearly every valuation metric whereas foreign stocks, in aggregate, offer much more attractive valuations.

Because starting valuation level plays such an important role in the forecast of 10-15 year expected returns, most institutions that produce long-term capital market assumptions show a notable difference in the return expectations of foreign stocks relative to US stocks. Although the nominal numbers in the forecasts below are different, the trend of foreign stocks having a significantly higher expected return over the coming decade is consistent.5

The Case for Overweighting US Stocks

Hedging – Revert back to the home country bias concept and the reality that most US investors are over-invested in US stocks. If your fellow neighbors are the ones competing with you for goods and services and they are all egregiously over-invested in US stocks, then the price of local goods and services is likely to be correlated with the rise and fall of US investments. The case for overweighting US stocks relative to their market capitalization weight is simply to hedge the possibility that US markets perform better than the rest of the world and that your purchasing power for scarce resources is diminished relative to your neighbors because of the biased mistake that everyone else is making.

Lower Transaction Costs – Another case for favoring US stocks relative to their market capitalization weight is that transaction costs and investment costs are higher for foreign investments. While still worth mentioning, these transaction costs were far more of an impediment to international diversification 40 years ago as the transaction cost-barriers to foreign investing have consistently declined over recent decades.

Debunking Lousy Excuses for Overweighting US Stocks and Underweighting Foreign Stocks

As we cover the possible justifications for under- or overweighting foreign stocks, it is appropriate to dispel several of the misguided arguments for favoring US stocks.

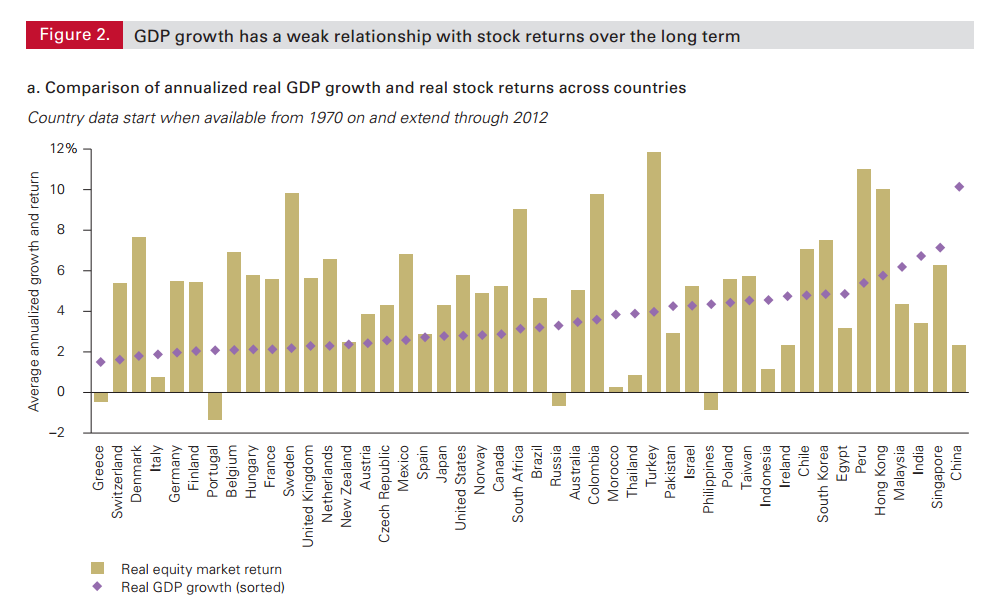

Europe and Japan are struggling with bigger issues than the US and. as a result, US economic growth is likely to be stronger and stocks returns higher. Among the most pervasively flawed investment concepts is the idea that measures like GDP growth or GDP/capita growth foretell investment returns. Despite the weak relationship between economic growth and stock returns, the concept continues to be promoted as it makes for an easy story. In fact, empirical evidence indicates that it works the opposite way – that there is a negative correlation between GDP growth and stock returns. As with individual stocks, it is actually the difference between consensus expectations and reality that best foretells future returns. Countries with high expected growth rates are priced to reflect lofty expectations. Vice versa for countries with low expected growth rates. Because there is a strong bias of investors to overpay for growth and erroneously extrapolate the recent past into the future, stocks in countries with low expected growth tend to outperform stocks in countries with high expected growth over long periods. The rationale of higher US growth and the resulting lofty expectations actually presents a compelling argument to underweight US stocks relative to their market capitalization, not overweight them.

Large US companies are multinational and get their revenues from around the globe. As a result, I get enough exposure to foreign markets simply by owning large US multinationals. Let’s start with the fatal flaw of this logic – it is completely arbitrary to only own multinationals that choose to headquarter in the United States. One might as well elect to only own multinationals that headquarter in states that start with the letter ‘N’. Diversification is the free lunch of finance and when there is a free lunch, you generally want as much lunch as you can get.

Second, being diversified in the stock market means more than just diversifying revenue streams. It means diversifying country-specific risks, industry-specific risks, and stock-specific risks. A negative corporate tax law change in the US negatively impacts companies headquartered in the US, irrespective of how diversified the revenues are. Owning Boeing (US based) but not Airbus (Netherlands based) means adding uncompensated company-specific risk that could easily be diversified. Buying only US-based automakers means ignoring most of the global luxury car market that is largely European-based. Buying only US-based companies means losing many benefits of currency diversification. This is all to say that US stocks provide global exposure but they don’t give the full benefit of global diversification.

US stocks have widely outpaced foreign stocks since the financial crisis due to the changing landscape and the innovation advancements of US-based companies like Amazon, Apple, and Google. Famously, the 4 most dangerous words in finance are said to be “this time is different.” The inescapable truth is that US stocks have outperformed foreign stocks over the past decade. But this is not unusual. US stocks have experienced extended periods of strong outperformance in the past. To suggest that this time is different makes a dangerous supposition. Strength of the US dollar over the past decade presents a future headwind for US companies just as weakness of foreign currencies over the past decade provide a future tailwind for those countries. The same can be said of lofty US valuations versus more attractive foreign valuations. There are persistent economic factors that drive the cyclicality evidenced below.6

Closing Thoughts – The Appropriate Foreign Mix

This is – to be clear – not just a fun thought exercise. Determining the mix of foreign stocks that belongs in a portfolio is one of the paramount decisions of portfolio management.

It is our humble belief that the global market capitalization provides the most useful starting point for this decision – one that best incorporates all the relevant information and a starting point that fits well with historical portfolio optimization evidence. There are reasonable cases to deviate towards a higher US stock allocation than the market portfolio or, conversely, towards a higher foreign stock allocation. That said, we believe that the current valuation divergence between US stocks and the rest of the world – one that is significantly elevated compared to history – presents the strongest case for tilting slightly above the 44.4% market capitalization weight for foreign stocks. History may not repeat itself – but it often rhymes. Valuations may not converge over the next week or the next year but we believe history will look unfavorably on investors who ignore the powerful historical tendency of valuations as a predictor of long-term returns.

{kind=link}