The relatively brief history of qualified charitable distributions (QCD) goes back to 2006 when Congress first authorized the QCD in the Pension Protection Act – but only for two years. It lapsed in 2008, 2010, 2012, 2014, and 2015, only to eventually be reinstated each time. In late 2015, Congress permanently reinstated the QCD. It was not until the Tax Cuts and Jobs Act of 2017 (TCJA) that consumers really started to take notice of the QCD. By dramatically increasing the standard deduction and limiting the deduction of state and local taxes, the TCJA significantly expanded the pool of QCD beneficiaries. Although public awareness of the QCD has grown since then, we find that many consumers are still not aware of the QCD or just do not understand the simplicity and benefits well enough to put it to use.

What is the Qualified Charitable Distribution?

Despite its lack of use, the qualified charitable distribution is not a complex tax planning vehicle or a tax strategy that only applies to a small fraction of taxpayers. The QCD rule simply permits taxpayers over age 70.5 to make IRA distributions directly to a public charity without treating the distributions as taxable income. That is, money goes directly from the IRA to the charity without passing go.

How Does the Qualified Charitable Distribution Work?

In the 1040 example below, note line 4. Under normal circumstances, this taxpayer with a $35,000 required minimum distribution reports 35,000 on line 4a (IRA distribution amount) and then the same 35,000 on line 4b (taxable amount). In this example, the taxpayer directed all of the $35,000 required distribution to charity which, in turn, meant that line 4b – the taxable amount – was $0. This has important ramifications, which will be explained later.

What are the Requirements of the Qualified Charitable Distribution?

There are several important (but easy to fulfill) qualifiers:

- The owner of the IRA must be at least age 70 ½ at the time of the distribution.

- The distribution must go directly to a public charity (not a donor advised fund or private foundation).

- The distribution must come from an IRA. Distributions from a 401(k) or 403(b) are not eligible.

- There is no minimum QCD amount but there is a $100k limit per individual taxpayer. Note that a married couple, both over age 70.5, each qualify for the $100k limit so they would be able to use up to $200,000, in aggregate.

What are the Tax Benefits of the Qualified Charitable Distribution?

Without the QCD, a taxpayer would take his or her required minimum distribution (RMD), donate the amount of the distribution to charity, and then take a charitable deduction to offset the income. In some cases, this would result in a perfect offset and no net impact to the tax liability. However, with more than 90% of taxpayers now claiming the standard deduction and many of the remaining taxpayers losing some of the itemized deduction benefit because of the increased standard deduction, the offset tends not to be dollar-for-dollar.

What is the Primary Benefit of the Qualified Charitable Distribution?

Some examples will help to answer this question.

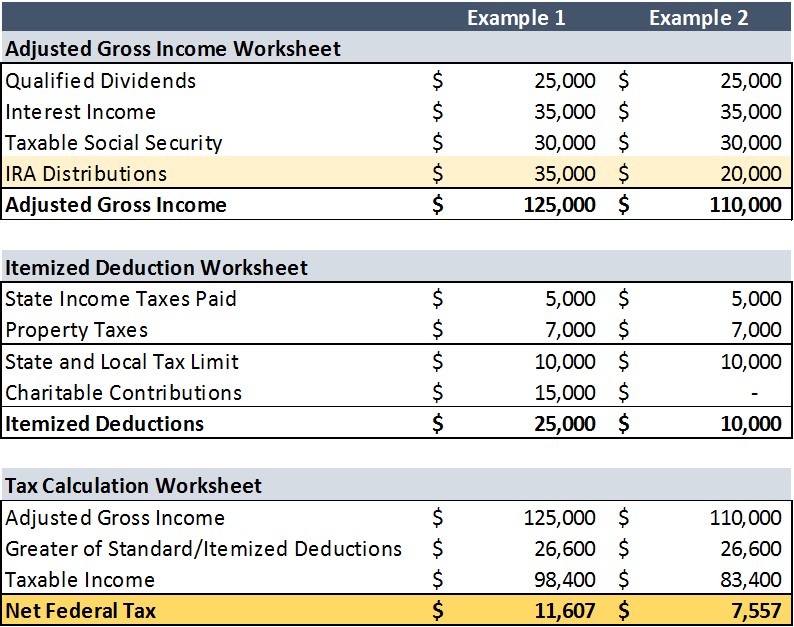

Example 1: Consider the case of a 72 year-old married couple, Jack and Diane, who have taxable Social Security income, dividends, and interest of $90,000 plus another $35,000 of required minimum IRA distributions from Jack’s IRA for total adjusted gross income of $125,000. They pay $5,000 of state taxes and $7,000 of property taxes, and have no mortgage or major medical expenses.

This year, they moved $35,000 from Jack’s IRA to their joint bank account to fulfill the required minimum distribution. Later in the year, they will write a check from their bank account for $15,000 to their favorite charity. Based on all their income and deductions, they will owe $8,444 in federal taxes.

Example 2: Now, assume everything stays the same except for the way in which Jack and Diane make their $15,000 charitable gift. Instead of moving $35,000 from Jack’s IRA to their bank account, they move $20,000 from the IRA to their joint bank account. Additionally, they give the same charity the same $15,000 but these funds come directly from the IRA. That is, the charity gets the $15,000 check directly from Jack’s IRA instead of going from Jack’s IRA to the bank account and then to the charity.

Financially, nothing changes for Jack and Diane and nothing changes for the charity. Check that – one thing changes for Jack and Diane. Instead of paying $8,444 in taxes in our initial example, they pay $6,644 in the second case. Their tax liability drops by $1,800 or 21.3% simply because they were wise enough to make use of the qualified charitable distribution.

What caused this significant reduction in federal taxes? In example 1, Jack and Diane made $15,000 of charitable contributions but they did not get any benefit from these contributions because their total itemized deductions of $25,000 were less than their standard deduction of $27,000. Had they given away $5,000, $10,000, or $15,000 or zero to charity, they would have faced the exact same federal tax liability.

In the second example, because they made the gift directly from their IRA and utilized the qualified charitable distribution, what would have been a taxable $35,000 mandatory IRA distribution was reduced to a $20,000 taxable distribution. In turn, their adjusted gross income and taxable income in example 2 were both $15,000 lower than in example 1. Yes, their itemized deductions were also $15,000 lower because they didn’t get to claim any charitable contributions but that’s the whole point. Reducing their income by $15,000 was far more valuable than increasing their itemized deductions by $15,000.

A married couple without major medical expenses or without a primary mortgage interest expense that exceeds $17,000 per year are likely to benefit from utilizing the qualified charitable distribution for the same reasons as Jack and Diane. It is a tax savings tool, unavailable to anyone under age 70.5, that effectively allows for the shifting of charitable deductions from the Schedule A, where they may not be entirely useful, to the front page of the Form 1040, where they’re going to be useful for anyone who pays taxes.

Who else might benefit from the QCD?

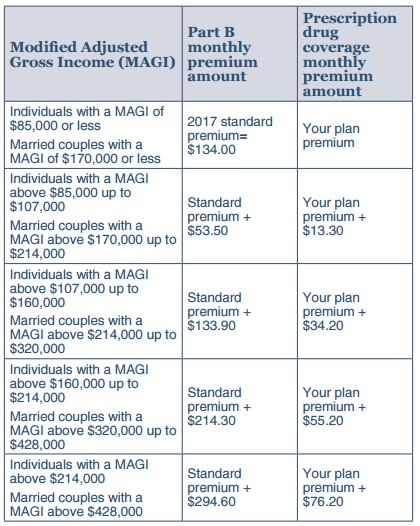

Couples with more than $170,000 of modified adjusted gross income and individuals with more than $85,000 of income can use the QCD to avoid higher Medicare premiums.

Medicare B and D premiums are tied to the modified adjusted gross income (MAGI) of taxpayers. Single taxpayers with modified adjusted gross income of more than $87,000 and married filing jointly taxpayers with MAGI of more than $174,000 pay an additional Medicare premium amount, known as income related monthly adjustment amounts (IRMAA). For example, a married taxpayer with modified adjusted gross income of $174,001 would pay an additional $115.60/month or $1,387/year compared to a couple with $174,000 of income – just $1 less.

The income thresholds in the leftmost column above are based on modified adjusted gross income – which means they are not reduced by itemized deductions (i.e. charitable gifts). A married taxpayer with $175,000 of adjusted gross income who donates $10,000 to charity via checks has to pay the higher Medicare premiums. However, if the same taxpayers use the QCD to donate the same $10,000 to charity, MAGI is reduced to $165,000 and the tax filer does not face the additional Medicare premiums – a simple and quick one year tax savings of $1,387.

Married tax filers with over $250,000 of AGI or single filers with over $200,000 of AGI can use the QCD to reduce the 3.8% Medicare tax.

The 3.8% Medicare tax on investment income only applies to married filers with more than $250,00 of AGI or single filers with more than $200,000. Utilizing the QCD technique can either relieve taxpayers of that tax completely by reducing AGI below those levels or can reduce the amount of investment income that is subject to the 3.8% tax.

For example, a taxpayer with $50,000 of charitable contributions who is subject to the 3.8% Medicare tax on $125,000 of income beyond the thresholds can save $1,900 in taxes ($50,000 x 3.8%) by simply making use of the QCD.

Rental property owners who actively participate in the property’s rental activity can use the QCD to qualify for a larger taxable rental loss.

If you own a rental property and meet the requirements to qualify for active participation (make management decisions related to the property, etc.), the tax code allows you to deduct up to $25,000 of rental property losses each year. Importantly, to claim the rental losses as an offset to other income, your AGI must be below $150,000 (or $75,000 for single filers). Since the income threshold is determined by AGI and not by taxable income, this presents another opportunity for the QCD to reduce income and, resultantly, to allow the taxpayer to claim a larger tax loss.

Tax filers who receive Social Security and have limited other income sources can use the QCD to reduce or eliminate the amount of Social Security that is subject to taxation.

The IRS looks at something called “combined income” to determine how much of your Social Security will be subject to taxes. Combined income consists of AGI (less Social Security) plus tax exempt municipal bond interest plus ½ of Social Security benefits. If your combined income is below $44,000 (for a married couple; or $34,000 for a single individual), then the amount of Social Security subject to taxation is reduced. Anyone close to these thresholds could benefit from utilizing the QCD to reduce combined income.

Tax filers who are constrained on the size of their charitable deduction can use the qualified charitable distribution to realize a larger tax benefit from their charitable giving.

For taxpayers who itemize deductions, the IRS limits the size of the charitable deduction to no more than 50% of adjusted gross income and, depending on other factors, sometimes 30% or 20% of AGI. As a result of these limits, taxpayers who make large charitable gifts each year can have their deduction limited. The QCD allows taxpayers to make charitable gifts without being subject to these limits.

Closing Comments

Importantly, none of the advice above suggests giving more dollars to charity simply for tax benefits. The amount of charitable giving is a personal decision that should not be determined or driven by potential tax savings. However, the method of gifting can often be optimized to have a profound impact on the tax benefit of the gift.

The intent here is not to suggest that the qualified charitable distribution has benefit for all individuals who are over age 70.5. In fact, the QCD is not going to be of any value for some tax filers. Individuals who do not make charitable gifts, who don’t fit any of the criteria above, or have large, low basis stock positions are likely not going to benefit from the QCD.

Instead, the intent here is to expand awareness on what the QCD is, how it works, and how you might benefit from its use. Simply understanding that it exists and how it can be utilized likely separates you from the majority of Americans.

2 Comments

[…] a quick refresher, the QCD (explained more fully in this Golden Bell article) was first authorized by Congress in 2006. It lapsed and was reinstated five times over the coming […]

[…] We think nearly every American over age 70.5 who donates any amount to charity should use the qualified charitable distribution (QCD) as a way to reduce taxes. We will keep driving this home until the QCD is a mainstream concept but […]

Comments are closed for this article!